In December 2025, the Russian Union of Industrialists and Entrepreneurs (RSPP) recorded a marginal decline in its composite Business Environment Index, which fell by 0.5 points to 46.1 points. The survey of industrial and business leaders revealed a notable softening in core economic activity, driven primarily by a contraction in demand.

The most significant pressure came from the Product Market Index, which dropped 3.6 points to 43.8. Respondents reported a marked decrease in both sector-wide demand and demand for their own products and services. The share of companies reporting reduced demand rose by approximately 10 percentage points compared to November. Consequently, the "industry demand" indicator fell sharply to 39.1 points from 45.5, while "demand for a company's own products/services" plummeted to 40.0 points from 49.2.

Input cost pressures persisted, with the "purchase prices" indicator falling to 28.5 points (-2.1), as nearly half of surveyed firms noted an increase. In contrast, selling price momentum weakened: the "selling prices" indicator fell 2.7 points to the neutral threshold of 50 points, with 68.2% of firms reporting stable prices. The proportion of companies raising prices declined to 16.5% from 19.2% in November.

Operational indicators presented a mixed picture. The "level of competition" component rose 1.9 points to 61.2, returning to its October level. However, the B2B Index declined by 2.2 points to 46.5, and "new order volume" fell 2.5 points to 51.8, with a growing share of companies (21.2%, up from 14.9%) reporting a decrease. The indicator for "fulfillment of obligations by companies" dipped into negative territory at 47.1 points, with a 5%-point increase in firms reporting more unmet obligations.

The logistics sector showed signs of stabilization. After two months of decline, the Logistics Index rose 2.9 points to 49.0. This was supported by a significant improvement in "inventory levels," which jumped 5.6 points into positive territory at 53.2. However, "average delivery time" remained a challenge, inching up 3 points to 48.5.

A notable bright spot emerged in external relations. For the first time in four years, the indicator for "relations with foreign partners" entered positive territory at 51.5 points, with 8.2% of companies noting an improvement. The B2G (business-to-government) Index also remained positive for the second consecutive month at 53.0 points, reflecting slightly more optimistic assessments of business-state relations.

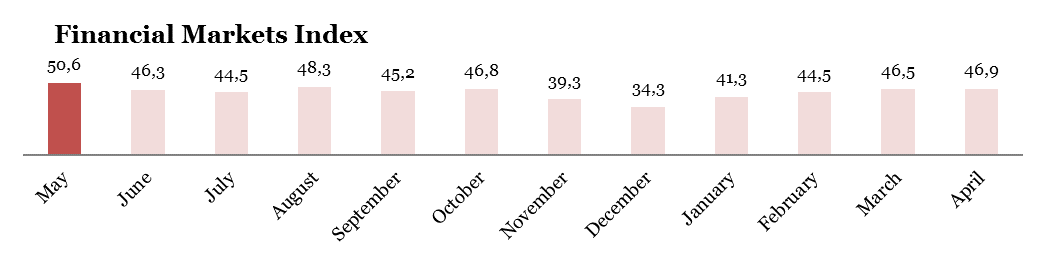

Financial market sentiment softened, with the corresponding index losing 1.1 points to settle at 45.4. The "financial position of companies" indicator declined to 41.8 points, as more firms (27.1%, up from 21.2%) reported a deterioration in their financial standing.

Social and Investment Activity, Stability Amid Challenges

On the investment front, 67.1% of companies maintained active investment programs, with two-thirds executing them without changes to schedule or budget. However, 14.5% were forced to reduce investment volumes, slightly outpacing the 12.5% that increased spending.

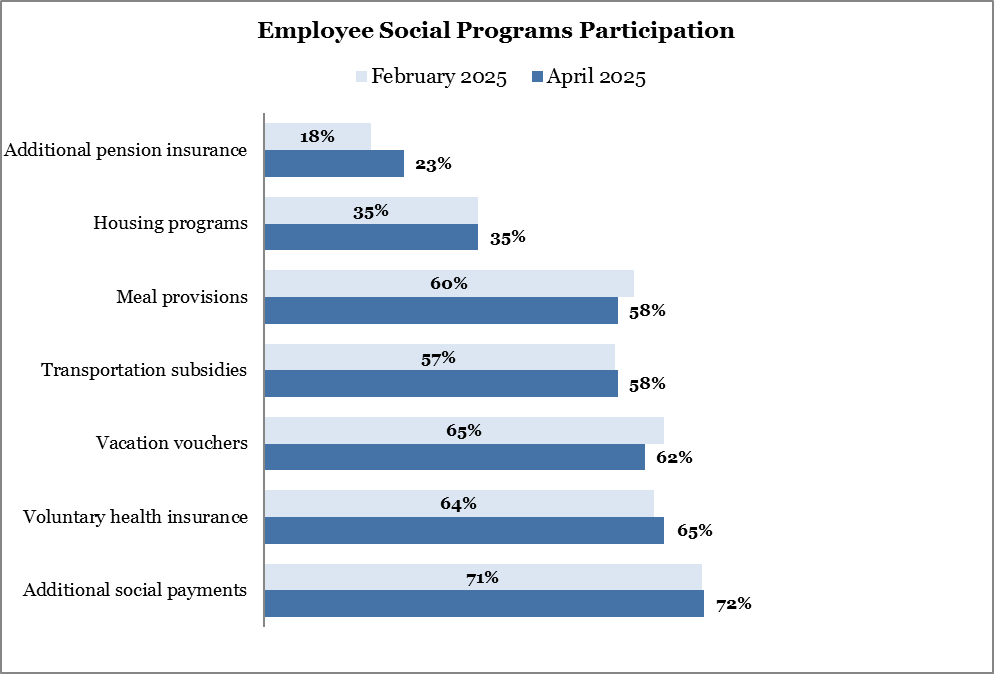

The labor market demonstrated resilience, with 77.6% of companies hiring new staff and only 9.4% reporting layoffs. A significant 89.4% of organizations maintained social programs for employees, the most common being subsidized resort/child recreation (71.1%), voluntary health insurance (64.5%), and extra-contractual payments to staff (59.2%). Budgets for these programs remained unchanged for 77.9% of firms.

Furthermore, 62.4% of companies participated in additional measures to ease labor market tensions, primarily through internships (49.4%) and advanced training programs (36.5%).

In summary, the December 2025 survey depicts a business environment dealing with weakening demand and financial pressures, offset by stable investment, a resilient labor market, and cautious optimism regarding logistics and certain external relations.

For more details, click

MOSCOW – Russia’s business environment showed tentative signs of stabilization in November 2025. According to the latest survey from the Russian Union of Industrialists and Entrepreneurs (RSPP), the key Composite Business Climate Index halted its decline, returning to its September level of 46.6 points. This apparent stabilization, however, conceals a more complex reality, where encouraging signals from core business operations are offset by enduring constraints in logistics and a cautious investment climate.

Improving Market Conditions and Pricing

The performance of the product market index rose by 1.8 points to 47.4. This was underpinned by a significant rebound in the B2B Index, which jumped 4.4 points to 48.7 after recently hitting a three-year low. Both demand within industries and for companies' own products saw positive shifts, with the latter nearing the 50-point threshold that separates contraction from expansion.

Pricing dynamics also improved. While purchase prices increased, the number of respondents reporting price hikes actually fell by 6%. More significantly, the sales price index entered positive territory, climbing to 52.7 points, suggesting companies are finding slightly more room to pass on costs.

Strengthening Contracts and Orders

Business reliability saw a marked improvement. The index for companies fulfilling their obligations surged 5.6 points to 51.6, re-entering positive assessment territory. Reports of growing unmet obligations halved, and a similar positive trend was noted for counterparties' reliability. This renewed confidence was reflected in new orders. The new orders index broke a two-month negative streak, leaping 6 points to a positive 54.3, driven by a 7.5% increase in companies reporting more orders.

Logistics and Competition: Emerging Pressure Points

However, not all signals were positive. The Logistics Index continued its gradual decline to 46.1 points. For the first time in two years, the assessment of warehouse inventory levels fell into negative (47.6 points), with fewer companies reporting improvements. This was partly offset by a slight improvement in overall logistics sentiment and delivery times. Furthermore, the competitive landscape intensified, with the level of competition index falling 2.1 points to 59.3.

Financial Sector and External Relations

The financial markets index showed a solid recovery, gaining 4.1 points to 46.5. Assessments of companies' own financial positions improved noticeably; the share of firms reporting a deterioration fell from over a quarter to a fifth, pulling the index up to 43.1 points. The stock market index also saw a sharp rebound of 6.6 points, as the number of negative assessments plummeted.

While the overall appraisal of relations with foreign partners remains marginally in negative territory, it improved significantly as the proportion of negative assessments fell by half.

Social and Investment Activity: A Mixed Picture

The social and investment sphere presented a contrasting view. On one hand, the proportion of companies running investment programs fell by 5.3 percentage points to 57.4%. However, among those investing, three-quarters reported sticking to their original schedules and budgets, and far fewer companies were forced to cut investment volumes.

Hiring remained robust, with 77.7% of companies recruiting, returning to September's levels. Social programs for employees were widespread (85.1% of companies), with the most common forms being extra-contractual payments, sanatorium vouchers, and private health insurance. For most companies (80.5%), social spending budgets remained unchanged.

To summarize, the Russian business landscape in November 2025 was characterized by a tentative recovery, driven by improved demand and operational reliability. Nonetheless, this progress remains vulnerable to enduring headwinds, most notably in the logistics sector, a highly competitive market, and a discernible pullback in corporate investment.

For more details, click

The Russian business environment deteriorated to its lowest point this year, according to the latest Business Climate Index from the Russian Union of Industrialists and Entrepreneurs (RSPP). The composite index fell to 44.3 points in October, signaling growing pessimism among industrialists and entrepreneurs, primarily driven by a worsening crisis in payment discipline between companies.

The survey results paint a picture of an economy facing internal strain, even as some external pressures have stabilized. The dynamics of demand were mixed: while perceived demand across entire industries fell, a slightly larger share of companies (20.3%) reported a rise in demand for their own products compared to those who saw an increase in broader sectoral demand (16%).

Deepening Corporate Illiquidity

The most alarming data comes from the B2B Index, which plummeted to a three-year low of 44.3 points. This decline is directly attributed to a sharp deterioration in the fulfillment of contractual obligations. The indicator measuring companies' own default rate fell by 5.6 points, while the metric for counterparties' defaults dropped 3.7 points to a very low 34.7 points. Crucially, the balance of responses shifted negatively: in October, 10% of firms reported an increase in their own unmet obligations (double the 5% that saw a decrease), and a full third of respondents reported a rise in defaults by their partners.

Logistics and Financial Pressures Mount

After five months in positive territory, the Logistics Index fell back into negative assessment, dropping to 46.5 points. This was largely due to a significant drawdown in warehouse inventories and longer average delivery times, suggesting companies are de-stocking amid uncertainty.

The financial outlook for companies also darkened. The "financial position of companies" indicator fell to 39 points, with over a quarter of respondents reporting a worsening of their financial health. The state of the stock market was assessed at 41.3 points, with 16.1% of businesses noting a negative dynamic and not a single respondent reporting an improvement. The only faint positive note in the financial sector was a slight stabilization in the currency market, which most companies (90.7%) described as unchanged.

Reflecting this challenging environment, the Personal Assessment Index fell to 36.9 points. A significant 31.3% of business representatives believe the country's business climate has worsened, while only 7.6% hold a positive view.

Investment and Social Activity: A Glimmer of Resilience

Despite the gloomy business climate, the data on corporate activity reveals a degree of resilience. Two-thirds of organizations continued to implement investment projects, with the majority (67.9%) doing so without changes to their schedule or budget. However, one-fifth of companies were forced to cut investment volumes.

The labor market showed strength, with 87.3% of companies reporting new hiring, a significant 12.3% increase from the previous period. Layoffs were reported by only 6.8% of organizations.

Social support for employees remains widespread, with 85.6% of companies maintaining such programs. The most common benefits are voluntary health insurance (66%), additional payments beyond legal requirements (63.1%), and subsidized vacation packages and children's camps (59.2%). For most companies (76.4%), spending on these social programs remained unchanged, though 14.5% managed to increase their budgets.

In summary, the October 2025 survey depicts a Russian business sector grappling with a severe internal liquidity crunch and logistical setbacks. While investment and employment have so far held relatively steady, the collapse in payment discipline and worsening financial assessments point to underlying vulnerabilities that threaten the economy's stability as the year draws to a close.

For more details, click

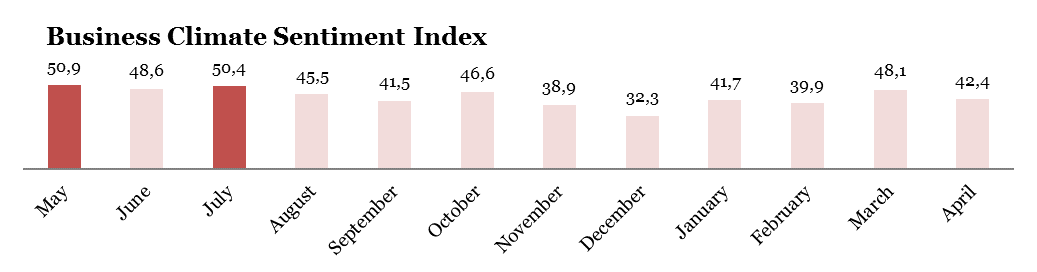

In September 2025, the Russian Union of Industrialists and Entrepreneurs (RSPP) released findings from its latest survey of industrialists and entrepreneurs, offering insights into the state of Russia's business landscape. The Composite Business Environment Index held steady at 46.6 points, a marginal increase from 46.5 points in August, signaling a stable yet cautious economic climate.

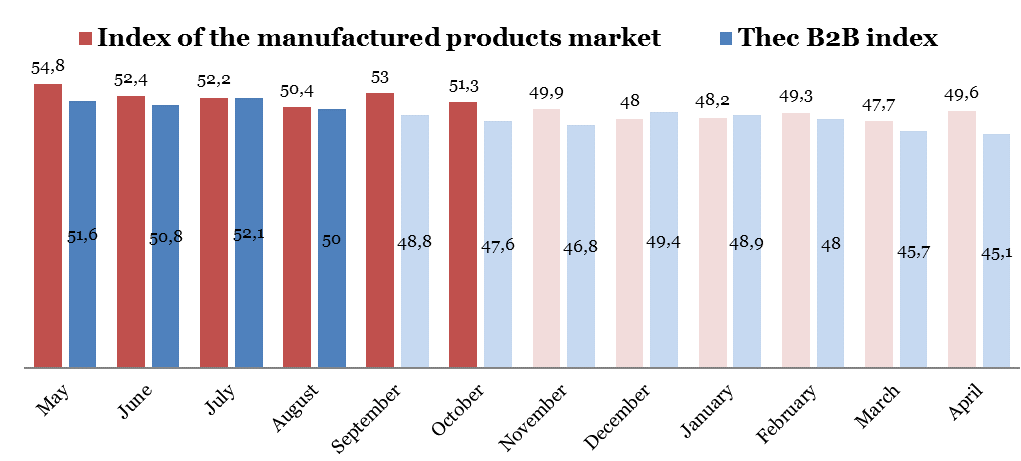

The Market of Manufactured Products Index saw a modest rise of 1.9 points to 45.7, driven by positive demand trends. Industry-wide demand improved notably, climbing 4.8 points to 46.2, with 21.4% of respondents reporting growth compared to just 14.8% in August. However, demand for individual company products grew more slowly, up 1.8 points to 44.2, with only 18.8% of businesses noting an increase. Procurement prices edged up slightly to 24.8 points, while sales prices dipped by 1.4 points, reflecting fewer companies raising prices. Competition intensified, with the level of competition indicator rising 4.4 points to 63.3, as a quarter of respondents observed heightened competitor activity.

The B2B Index slipped slightly to 46.4 points from 46.9 in August. New orders weakened, falling to 45.5 points, with 23.2% of companies reporting a decline compared to 17.7% the previous month. On a positive note, production timelines improved, reaching a neutral 50 points, up 2.8 points. The fulfillment of obligations to counterparties remained solid at 51.6 points, though a persistent 13.2-point gap highlighted challenges in counterparty reliability, with nearly 30% of firms noting increased unfulfilled obligations.

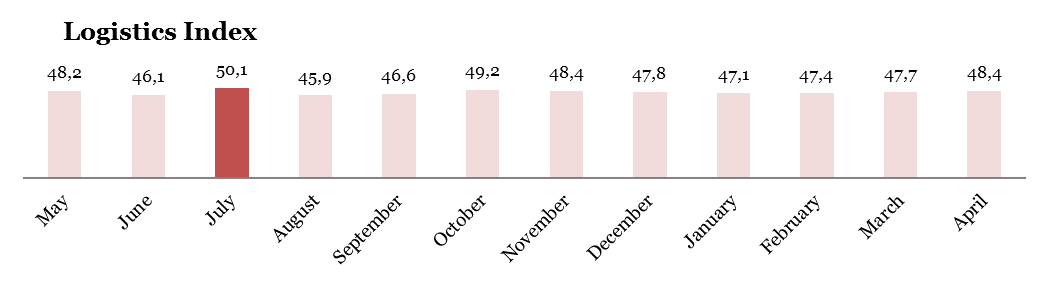

Logistics showed resilience, with the Logistics Index holding in positive territory at 50.7 points for the fifth consecutive month. Warehouse stock levels stood at 57.4 points, with one-fifth of companies reporting increases. Delivery times improved marginally to 47.1 points, with 5% of firms reducing delivery times compared to 2.8% in August. Overall, the logistics sector's outlook brightened, with its assessment rising by 1.9 points.

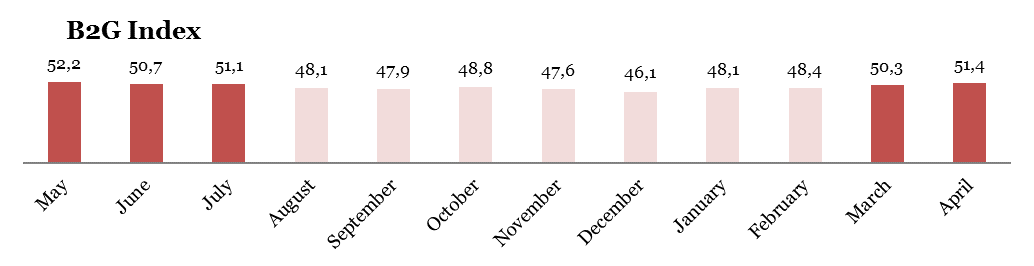

The B2G Index, reflecting business-government relations, remained stable at 51.6 points. Approximately 85% of respondents reported no significant changes in ties with financial institutions or government bodies, though nearly 10% noted slight improvements. Relations with foreign partners saw a more positive shift, with the indicator rising from 47.9 to 49.1 points.

The Financial Markets Index stayed nearly flat at 44.5 points. However, the financial position of companies deteriorated slightly to 41.7 points, with 26.8% of firms reporting a worsening situation, up from 20% in August. Stock and currency market indicators showed minimal change, rising to 46 and 45.8 points, respectively, with over 85% of respondents viewing these markets as stable.

Personal assessments of the business climate took a hit, dropping 2.6 points to 40.5, with 30.4% of respondents noting a decline, a 6% increase in negative sentiment. Investment activity remained consistent, with 63.4% of companies engaged in projects, two-thirds of which proceeded on schedule and within budget. However, a quarter of firms lagged behind, and one-fifth reduced investment budgets, though 13.9% increased spending.

Hiring trends softened, with 75% of companies recruiting, down from 80% in August and 85% earlier in the year. Layoffs rose, affecting 10% of firms, up 7% from prior months. Cost-cutting measures, such as reduced working hours, were implemented by 10.8% of organizations. Social programs remained robust, with 80.4% of companies supporting employees through benefits like spa vouchers (69.2%), additional payments (67%), and voluntary health insurance (62.6%). Nearly half of the firms also supported broader community initiatives.

The September 2025 survey paints a picture of a business environment marked by cautious optimism, with gains in logistics and competition offset by softening demand, financial pressures, and declining confidence.

As companies navigate these dynamics, the focus on investment and social programs underscores a commitment to resilience amid uncertainty.

For more details, click

In August 2025, Russia's business environment exhibited signs of cautious optimism, with the overall Composite Index edging up by 0.7 points to 46.5, according to a survey by the Russian Union of Industrialists and Entrepreneurs (RSPP). Despite this slight improvement, the index remains below the 50-point threshold, indicating that a negative assessment continues to prevail among businessmen.

The landscape of demand presented a contradictory picture. While perceived demand within industrial sectors saw an improvement, the demand for companies' own products and services fell significantly. This decline is attributed to a notable increase in the number of respondents reporting a drop in orders for their goods. The pressure on businesses continued from the cost side, with a majority of 51.8% reporting rising input prices, causing the corresponding index to fall. In contrast, selling prices remained largely stable, hovering in slightly positive territory.

Operational indicators were mixed. In a positive development, the volume of new orders received by companies crossed into positive territory for the first time, marking a significant monthly improvement. However, companies reported a slight easing in competitive pressures and a minor lengthening in order fulfillment times. The logistics sector sent conflicting signals; while warehouse inventory levels rose substantially and the overall logistics index was stable, qualitative assessments of the logistical situation itself worsened, with more businesses reporting deterioration than improvement.

A notable bright spot was the relationship between businesses and the state. The B2G Index returned to positive ground, driven by a slight preponderance of positive over negative responses regarding interactions with both financial institutions and government bodies. Financially, companies reported a modest improvement in their own financial positions, though perceptions of the stock and currency markets remained neutral to negative. This contributed to a significant jump in personal optimism, with the index of personal assessments rising sharply as negative views on the country's business climate contracted.

Beyond immediate business concerns, the survey revealed robust investment and social activity. Nearly two-thirds of respondents were actively pursuing investment projects, and crucially, a overwhelming 82% of them were doing so without any delays or budget overruns—a significant increase from the previous month.

The labor market appears stable, with an overwhelming majority of companies hiring and only a small fraction reporting layoffs. Social programs for employees are widespread, with 86.1% of companies offering benefits such as extra payments, health insurance, and vacation vouchers. Most companies held their social spending steady, and a strong majority also engaged in additional measures to support the labor market, primarily through employee internships and advanced training programs.

In summary, the August 2025 data paints a picture of an economy finding a fragile equilibrium. Businesses are navigating persistent cost pressures and uneven demand but are responding with stable investment, hiring, and social support, all while expressing a slightly more optimistic outlook for the future.

For more details, click

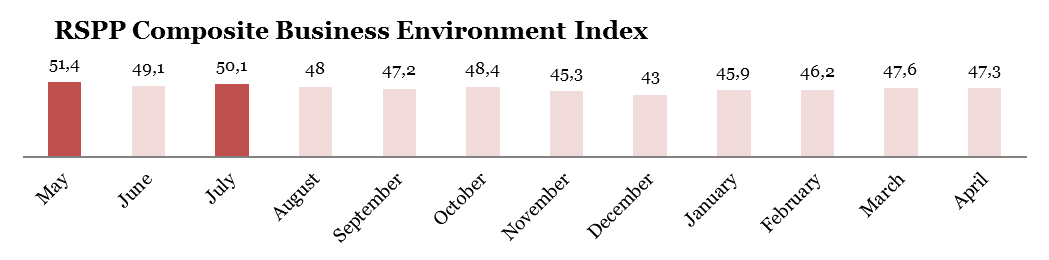

The latest survey by the Russian Union of Industrialists and Entrepreneurs (RSPP) reveals a slight deterioration in business sentiment during July 2025, with the composite Business Environment Index declining by 1.4 points to 45.8 points. This downward trend reflects growing caution among industrialists and entrepreneurs, driven primarily by weakening demand and ongoing price pressures. While selling prices showed modest improvement, rising to 51.1 points and re-entering positive territory, purchase prices remained depressed at 28.5 points despite nearly half of surveyed firms reporting continued cost increases. The B2B sector remained stagnant, with new orders dropping further to 46.8 points, indicating persistent challenges in securing business.

Logistics performance presented a mixed picture. Although the Logistics Index maintained its positive trend for the third consecutive month at 50.4 points, delivery times worsened significantly, with the indicator falling to 44.1 points. Nearly 14% of companies reported longer shipping delays, up sharply from 6.8% in June. Meanwhile, government-business relations showed volatility, with the B2G Index slipping to 49.2 points, just below the neutral threshold. Financial market sentiment also softened, with the Financial Markets Index dropping to 44.1 points as companies expressed greater concern about their financial positions.

On the investment front, two-thirds of surveyed enterprises maintained their capital expenditure programs, with most reporting adherence to original schedules and budgets. However, nearly 20% were forced to scale back investments, outweighing the 4.5% that increased spending. The labor market demonstrated resilience, with 85% of firms continuing to hire, though a small but notable 7.5% implemented layoffs or reduced working hours. Social programs remained widespread, with 84% of companies offering employee benefits ranging from healthcare support to housing assistance. The vast majority of companies kept social budgets unchanged, signaling stability in corporate welfare commitments despite broader economic headwinds.

The business climate faces challenges from softening demand, supply chain disruptions, and strained foreign partnerships. However, the sustained investment activity and robust employment figures suggest underlying resilience in Russia's industrial sector. The coming months will prove critical in determining whether these stabilizing factors can offset the prevailing negative trends in business sentiment.

For more details, click

In June 2025, the Russian Union of Industrialists and Entrepreneurs (RSPP) released its latest survey on the country’s business climate, revealing a mixed yet cautiously optimistic outlook. The Composite Business Environment Index rebounded to 47.2 points, matching its April level after a 1.8-point monthly increase. While certain sectors demonstrated resilience, others faced persistent challenges, reflecting the complexities of the current economic landscape.

The product market index declined to 44.7 points, marking a 1.1-point drop from the previous month. This downturn was primarily driven by two key factors: a historic low in sales prices (49.3 points, the weakest since July 2020) and a notable decrease in perceived competition levels (61.5 points, down by 6.9 points). However, demand conditions showed modest improvement, with both industry-wide and company-specific demand indicators rising by 2 points. Additionally, companies reported fewer concerns over procurement costs, as the share of negative responses fell by 3.5 percentage points, pushing the corresponding index up to 29.5 points.

The logistics sector remained in positive territory, with the overall index holding steady at 51.4 points. Despite this stability, underlying metrics revealed some strain: average delivery times and inventory levels both dropped by over 2 points, settling at 46.6 and 58.6 points, respectively. Encouragingly, broader perceptions of logistics conditions improved, with the sector sentiment index climbing 3.1 points to 49 points. This shift was attributed to a growing share of respondents reporting logistical improvements—a sign that supply chain bottlenecks may be easing.

The B2B sector saw a slight uptick, with its index rising to 46.1 points (+0.5). However, a concerning development emerged in new orders, which fell into negative territory for the first time in three years (49.3 points, down 2.6 points). This decline coincided with a 5-percentage-point reduction in companies reporting increased order volumes. In contrast, the B2G (business-to-government) index staged a strong recovery, jumping 4.8 points to 51.8. Notably, not a single respondent described government relations as deteriorating—a stark improvement from May’s results.

Financial pressures on businesses appeared to ease slightly, with the financial position index climbing to 44.2 points (up from 41.7 in May). The share of firms reporting worsening conditions dropped from 25% to 20.5%, signaling tentative stabilization. Meanwhile, investment activity remained steady, with over 63% of companies continuing their programs—71.2% of which adhered to original schedules and budgets. Nevertheless, one-fifth of firms reduced investments, underscoring lingering caution.

Employment trends remained robust, with 83.6% of surveyed organizations actively hiring and none reporting layoffs. Companies also maintained strong social commitments: 93.2% ran employee support programs (including bonuses, healthcare, and housing aid), while 76.7% participated in labor market initiatives like retraining and temporary employment schemes. These efforts reflect a corporate emphasis on workforce stability amid economic fluctuations.

For more details, click here